Low inflation, low interest rates, high growth rates, deeper financial inclusion using technology.

On these four core policy thrusts will public management expert and political economist Benjamin E. Diokno, 71, be remembered by the Filipino people as governor of the Bangko Sentral ng Pilipinas (BSP).

The central bank chief thinks the inflation rate or the rate of increase in prices of goods and services consumed by an average Filipino household will be 2.9% for the whole of 2019.

In September and October of 2018, inflation climbed to 6.7%—the highest in 11 years, thanks to the state-owned National Food Authority (NFA) announcing a rice shortage before it happened and NFA, given P5 billion, deciding to pay its debts instead of buying rice to boost the stockpile of the Filipino staple food.

Rice is 15 points of a poor man’s consumer price index (CPI or the basket of goods and services). Together, all food items account for 50% of that CPI. Since rice is a bellwether food item, when its price goes up, so do prices of other food items. Since food prices have psychological effect on all other products, the price of all other products rise as well. Worsening the situation last year was the sudden spike in prices of refined petroleum products, thanks to TRAIN.

Diesel used to be zero excise tax per liter. It was taxed at P2.50 per liter in 2018; P4.50 by January 2019. The government claimed diesel is dirty and is used mainly by the rich. Not true. Diesel is used by farmers for irrigation, by fishermen for their fishing boats, by drivers for their jeepneys, the main transport of the poor. Diesel is also a bellwether product. You increase its price with a tax, you increase the prices of other commodities.

The government now allows private companies to import rice. Rice imports are no longer limited by quotas, but by tariffs, meaning as long as the importer pays tariffs, he can import as much rice as he can. The result: A flood of imported rice, bringing rice price down from P50 per kilo to as low as P27. If you halve the price of rice and rice is 15 points of the CPI and all food is 50% of the CPI, you readily reduce inflation by at least 25%. In fact, inflation by April 2019 was cut by half to 3% or less than half of the 6.7% September-October 2018 inflation. Diokno thinks inflation for the whole of 2019 will be 2.9%, if not lower.

How will Diokno cut interest rates? He will flood the banking system with money. How? By lowering the reserve requirement (RR) on bank deposits. Reserve is the percentage of deposits banks must park with the central bank. It is useless, idle money.

You release it to the system by lowering the reserve requirement, initially, from 18% when Diokno took over BSP governor last March 2019, to 16%, a reduction of two percentage points. One percentage point is equivalent to P100 billion. Two percentage points is P200 billion.

With reserve at 16, only P84 billion of each P100 billion will be released to the system. So P200 billion less 16% reserve is P168 billion. Usually, banks can lend a peso of deposit 7x, assuming their capital can handle the risk, so 7x P168 billion is P1.176 trillion.

Over the next four years of his governorship, Diokno promises to cut RR by half or to 9%, in effect releasing P900 billion which the banks will have to lend as loans – to corporations (including government), to consumers, to you and me.

If there is more supply of money, interest rates (which is the price of money) will go down. The cheaper money borrowed then will go into capital goods (roads, bridges, machinery and equipment, cars, your smart), and consumption (shopping at SM, travel abroad, trip to Tagaytay, dining at Mang Inasal). Businesses will expand. Government will improve infra. More factories will be opened and more people will be hired. So good times are ahead.

Diokno notes that other countries in ASEAN have even lower RR. Thailand is 1%. Malaysia is 3.5%. No wonder these countries are robust, economically. Their economy is flooded with deposit money.

With the spending buoyant and the economy expanding, you have high growth rates.

This is not happening yet though. In fact, economic growth as measured by GDP growth rate, is slower—from 7.2% in third quarter (Q3) 2017, 6.5 in Q4 2017, 6.6 in Q1 2018, 6.2 in Q2 2018, 6 in Q3 2018, 6.1 in Q4 2018, and finally, down to 5.6% in Q1 2019.

Why the slowing growth? I suspect government people are stealing the money (the so-called corruption) or are simply incompetent to implement projects (the so-called absorptive capacity). And private companies have been slow to react to the improved economic environment (the so-called economic lag of projects).

How can the poor benefit from all this good news?

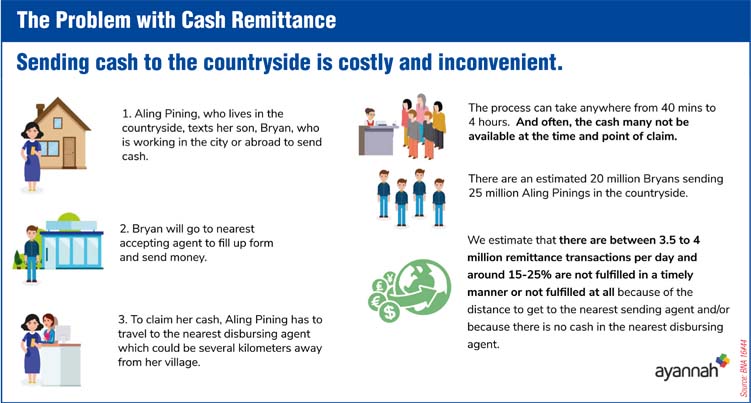

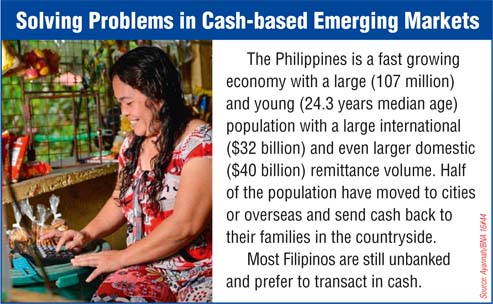

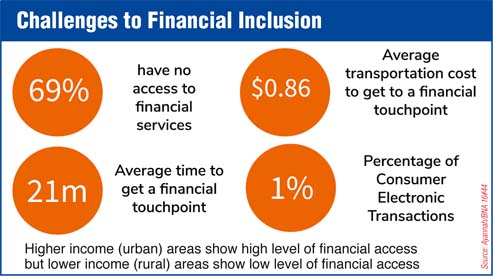

That is where financial inclusion comes in. Banks will pay more attention to you. Some 600 towns have no banks. BSP explains financial inclusion this way:

“Financial inclusion is a state wherein there is effective access to a wide range of financial services for all. Effective access does not only mean that there are financial products and services that are available. These products and services must be appropriately designed, of good quality and relevant to benefit the person accessing the said service. Wide range of financial services refers to a full set of products such as savings, credit, insurance, payments and remittance services for different market segments, particularly those that are traditionally underserved or unserved.”

Diokno hopes to achieve financial inclusion thru technology – thru your cellphones, Facebook, the internet of things, the digitalization of banking functions. You get your remittance thru your cellphone. You pick up your money from 7-11, Jollibee, Mcdo, Starbucks, your corner pawnshop. You pay your bills thru them too. Kasama ka, kasali ka. Sa pera ng bangko.